Dear friend, the following is our monthly market report update, for your reference.

1. Tinplate Price Movements

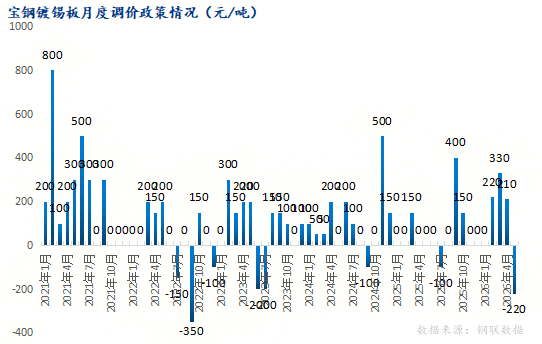

Baosteel, Wugang, and Meigang lowered tinplate prices by RMB 220/MT, due to falling tin prices; chromium-coated steel prices remained unchanged.

Other producers saw minor fluctuations or no changes.

Raw materials:

-

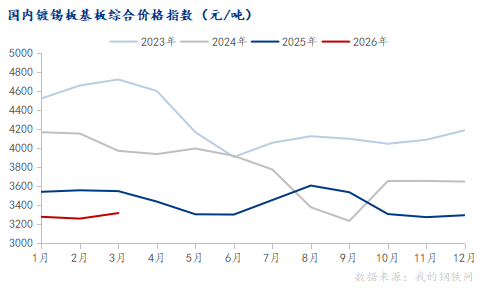

Tinplate base sheet: slightly increased

Raw materials:

-

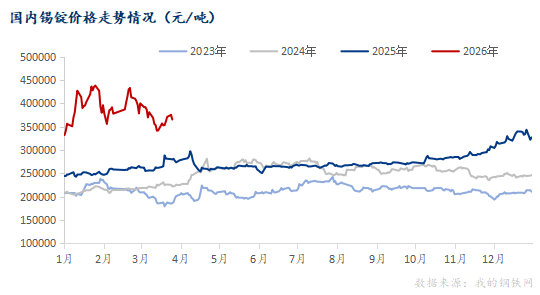

Tin ingot: prices temporarily fell, affecting tinplate price

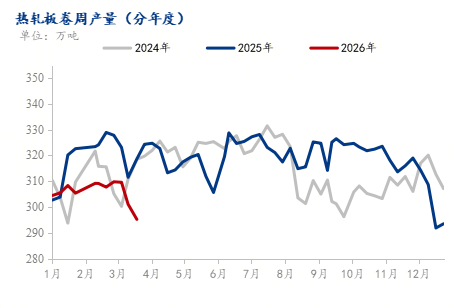

2. Hot-Rolled Coil Market

Post‑Spring Festival, total finished steel inventory pressure is not severe, and destocking is normal, though structural pressure remains. Strong coil and export orders keep high inventory from fully suppressing prices. The first round of coke price hikes and modest increases in steel output support costs.

As of March 25, 2026:

-

64 production lines among 37 surveyed mills: 50 active (78.13% utilisation, flat weekly).

-

Capacity utilisation: 78.18% (+1.38% WoW).

-

Daily output affected by maintenance: 32.6 kt (-0.3 kt WoW); by underfeeding: 39.2 kt (-6.8 kt WoW).

-

Actual weekly production: 3.0561 Mt (+54 kt WoW).

-

Mill inventories: 838.5 kt (-11.1 kt WoW).

-

Commercial coil: 2.0988 Mt (+54.3 kt WoW); internal supply: 957.3 kt (-0.3 kt WoW).

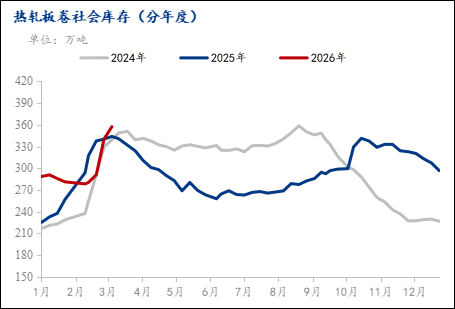

As of April 2, social inventories of hot-rolled coils in 33 major cities stood at 3.5888 million tonnes, down 105,400 tonnes week-on-week and 227,300 tonnes month-on-month, but up 577,900 tonnes year-on-year. In 55 major cities, inventories were 4.9886 million tonnes, down 79,200 tonnes week-on-week and 201,000 tonnes month-on-month, up 773,500 tonnes year-on-year. The total for key cities nationwide was 7.156 million tonnes.

Outlook: Downstream and export orders remain stable. High absolute inventories cap price upside, while resilient external demand supports normal destocking. Downside risks would likely come from macro factors (e.g., geopolitical energy shocks). Without major demand surprises, prices are expected to range sideways. If a US‑Iran ceasefire is reached in early‑mid April, energy prices may ease, limiting black steel upside.

3. Tinplate Production

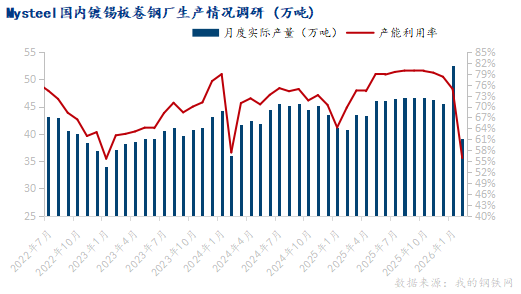

March 2026 (Mysteel survey of 30 tinplate producers):

-

Operating rate: 83%

-

Capacity utilisation: 72.89%

-

Actual output: 511 kt (+30.46% MoM)

-

Same‑sample mill inventory: 232.4 kt (-2.3 kt MoM)

Chromium‑coated steel output (domestic key producers): 135.9 kt (+14% MoM).

4. Downstream & Trade

4.1 Tinplate Exports

-

Feb 2026: Tinplate exports 139.6 kt (+1.85% YoY); Jan‑Feb total 285.2 kt (+0.05% YoY).

-

Feb 2026: Chromium‑coated steel exports 48.2 kt (+38.48% YoY); Jan‑Feb total 77.4 kt (-8.26% YoY).

Full‑year 2025 tinplate exports grew 16.17% YoY. Early 2026 maintained growth, but March may weaken due to geopolitical conflicts.

4.2 Beverage Production (Jan‑Feb 2026): 26.751 Mt (-0.36% YoY).

4.3 Dairy Products (Jan‑Feb 2026): 5.133 Mt (-12.94% YoY).

4.4 Packaging Industry (2025, China Packaging Federation):

-

Revenue: RMB 2,054.63 bn (-2.35% YoY)

-

Profit: RMB 95.15 bn (-1.69% YoY)

-

Trade: total $52.317 bn (+$101.9 mn YoY); imports $6.908 bn (-2.79%); exports $45.409 bn (+2.76%).

4.5 Shougang Jingtang published the English version of its EPD for electro‑tinplate, the first such English EPD for Chinese tinplate. This gives Chinese premium metal packaging materials a “green passport” for global markets.

5. Trade Policies

-

Vietnam: Anti‑dumping duties of 23.10%–27.83% on Chinese HRC (effective July 6, 2025, for 5 years). Anti‑circumvention investigation launched Oct 27, 2025.

-

EAEU: Safeguard investigation initiated on tinplate (width ≥600mm, thickness <0.5mm, tin coating >97%). May lead to extra duties.

-

Brazil: Five‑year anti‑dumping duties on coated steel from China and India. Existing measures on various steel products. Tinplate remains under monitoring for Germany, Japan, Netherlands.

-

Thyssenkrupp Rasselstein: Launched tinplate cans based on bluemint® reduced‑carbon steel (62% lower CO₂ emissions) in cooperation with Henkel and Pirlo – a benchmark in green transition.

-

EU CBAM: Stricter carbon reporting for imported steel (incl. HS 7210) now effectively a trade barrier; detailed carbon footprint data required

Outlook for April

Short‑term tinplate prices may dip due to falling tin ingot prices, but spring demand and supportive policies under the 15th Five‑Year Plan should help most steel prices rebound. Tinplate prices are expected to remain firm, with some specifications returning to rational levels.

We look forward to discussing future opportunities with you in person. RIC PACKAGE invites you to METPACK 2026, where we will showcase new products, technologies and solutions to address raw material sourcing challenges and tariff/trade barriers, enhancing your brand’s competitiveness. Contact us now to schedule a visit and get support.

www.ricpackage.com

DATA FROM@mysteel.com