Dear friend, the following is our monthly market report update, for your reference.

Theme: Significant price increases have been observed across major steel producers and raw materials.

1.Tinplate Price Changes:

Tinplate & TFS (Tin-Free Steel)

Baosteel (including Meishan Steel, WISCO): Tinplate prices increased by 210 RMB/ton, and TFS prices increased by 100 RMB/ton.

Cumulative Increases (2026): Since the start of 2026, Baosteel has raised prices by 220 RMB/ton in January, 330 RMB/ton in February, and 210 RMB/ton in March.

Total Impact: The total 2026 increase of 760 RMB/ton represents a jump of over 10%, primarily driven by rising tin metal prices. When including the price hikes from late 2025, the total increase exceeds 15%.

Private Mills: Other private steel mills have increased prices by 100–150 RMB/ton, with cumulative 2026 increases reaching 500–700 RMB/ton (over 10%).

Baosteel Price Adjustment Record Table:

Major producers have implemented a uniform price hike for hot-rolled steel:

Baosteel, Ansteel, Bensteel, and Lingsteel: All reported price increases of 200 RMB/ton

2. Raw Materials (Tin Ingot)

2.1 Spot Prices:Tin ingot prices are currently fluctuating, with a recent quote of 372,940.00 RMB/ton.

2.2 Analysis of the Impact of Middle East Conflict on China’s Tinplate Supply

The impact of the Middle East conflict on China’s tinplate exports does not primarily stem from the Iranian market itself (as exports to Iran are minimal, accounting for only 0.17%), but rather from the logistical disruption to core Middle Eastern markets such as the UAE and Saudi Arabia caused by potential blockades in the Strait of Hormuz.

Market Importance:

The Middle East region (including the UAE, Turkey, Saudi Arabia, and three other countries) accounts for approximately 20.35% of China’s total tinplate exports, making it a crucial export region.

Short-Term Logistical Paralysis:

Operations at Jebel Ali Port in the UAE, the largest port in the Middle East and a core transit hub for China’s steel exports (handling about 50% of China’s imports destined for the region), have been suspended.

While cargo can potentially be diverted to other ports like Fujairah and Sharjah, this will likely lead to severe congestion that will be difficult to alleviate in the short term.

Soaring Costs:

Freight Rate Increases: Shipping lines are imposing surcharges (like GRR) or suspending routes.

Oil Price Pass-Through: The Strait of Hormuz is a vital global energy artery; if oil prices rise due to the conflict, it will further increase shipping costs.

Higher Insurance Premiums:This will significantly increase the landed cost of imported goods.

Current Market Situation:

Short-Term: Orders for early-to-mid March, placed in February, have not yet been significantly impacted.

Medium-Term: New orders placed in March and exports scheduled for April onwards will directly face the crisis. Currently, freight rates are generally rising, buyers in the Middle East have stopped inquiring, and some exporters have been forced to stop quoting due to the uncertainty, bringing the market to a standstill.

One-Sentence Summary:

The Middle East conflict, by causing key port closures and freight rate spikes, is placing China’s tinplate exports to the region under the dual pressure of declining shipment volumes and rising landed costs in the short term.

3. Supply and Export Data

3.1 Exchange Rate: The USD/CNY exchange rate has dropped from 7.3 (July 2025) to approximately 6.85, affecting FOB export prices by roughly 6.5%.

3.2 China Annual Export Data

According to statistics from the China Packaging Federation, from January to December 2025, there were 20,230 packaging enterprises above designated size nationwide: Their cumulative operating revenue was RMB 2,054.627 billion, a year-on-year decrease of 2.35%; the cumulative total profit was RMB 95.152 billion, a year-on-year decrease of 1.69%. From January to December 2025, the total import and export value of the national packaging industry was USD 52.317 billion, an increase of USD 1.019 billion compared to the same period last year. Among this, imports were USD 6.908 billion, a year-on-year decrease of 2.79%; exports were USD 45.409 billion, a year-on-year increase of 2.76%.

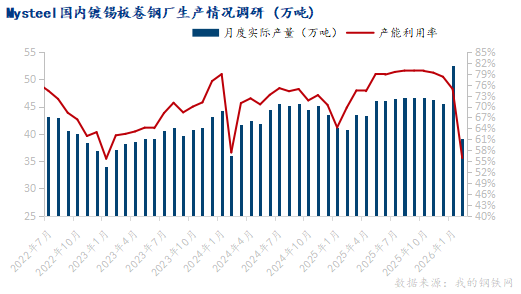

3.3 Tinplate Supply Decline in February

Based on monitoring data from 30 tinplate production enterprises:

Operating rate in February 2026: 79.25%

Capacity utilization rate: 55.87%

Actual tinplate production in February: 391,700 tons, a month-on-month decrease of 25.3%.

Inventory in the same sample factories: 234,700 tons, a month-on-month increase of 6.78%.

In addition, data from a survey of key domestic TFS production enterprises show that TFS production in February totaled 119,200 tons, a month-on-month decrease of 21.27%.

3.4 Export Data

Tinplate: Total exports in December 2025 were 142,900 tons, a year-on-year increase of 1.90%; total exports from January to December 2025 were 1.9903 million tons, a year-on-year increase of 16.17%.

TFS (Chrome-plated): Total exports in December 2025 were 37,300 tons, a year-on-year increase of 4.47%; total exports from January to December 2025 were 561,300 tons, a year-on-year increase of 25.56%.

TFS Imports: There were no imports of TFS in December 2025; total imports of TFS from January to November 2025 were 1,050 tons, a year-on-year decrease of 78.92%.

3.5. Brazil Anti-dumping Case

On March 2, 2026, the Secretariat of Foreign Trade of the Ministry of Development, Industry, Trade and Services of Brazil issued Announcement No. 16 of 2026, making an affirmative preliminary anti-dumping ruling on tinplate (chrome-plated steel sheet/coil) originating from Japan, Germany, and the Netherlands (Portuguese: folhas metálicas). It recommended continuing the investigation without imposing provisional anti-dumping measures and extended the deadline for the final ruling in this case to within 18 months from the initiation of the investigation. The products involved fall under Mercosul Common Nomenclature (NCM) codes 7210.12.00, 7210.50.00, 7212.10.00, and 7212.50.90.

Summary and Recommendations

According to current market feedback, hot-rolled coil, coke, coal, tin metal, and other bulk commodities are all experiencing price increases. Coupled with exchange rate fluctuations and the surge in freight rates and surcharges caused by the conflict, cost increases for end customers have become unavoidable. These costs will likely be passed down the supply chain quickly, affecting the end-user market.

We recommend considering the procurement cycle in advance, locking in purchase prices early, and coordinating closely with logistics teams to avoid disruptions to production.

The RIC team is currently encountering several situations involving passively increased prices for shipments, goods held up at third-party ports, and shipments that cannot be dispatched. If you require any assistance, our team is ready to offer any possible advice and support.

www.ricpackage.com

DATA FROM@mysteel.com